Introducing Elston Retirement Income Solutions

- Our Retirement Income Solutions framework is available for licensing to discretionary managers and financial advisers to help deliver advisers' Centralised Retirement Proposition ("CRP").

- It combines purpose-built bucket-based Retirement Portfolios with an Annuity Glidepath - a ladder of later-life annuity purchased as clients age.

- Drawdown first, then annuity later provides an optimal “blended” retirement income solution. A longer drawdown means greater flexibility and potential for growth. A later annuity means greater peace of mind and fewer complex decisions.

About the solution

The solution consists of:

- Purpose-built retirement portfolios

- An Annuity Glidepath

- Retirement Pathways and Cashflow Modelling integrations

About this solution

Combining a retirement portfolio in drawdown with an “Annuity Glidepath” combines flexibility, with peace of mind.

Our Retirement Income Solution is designed to assist DFMs and financial advisers offer a comprehensive retirement income solution to their clients as part of their Centralised Retirement Proposition.

The Annuity Glidepath blends a purpose-built retirement portfolio in drawdown with a ladder of later-life annuities to create a blended retirement income solution for clients, as part of a Centralised Retirement Proposition.

When considering retirement income recommendations, advisers have been faced with considering recommending either drawdown or an annuity. Now it’s not an either/or decision.

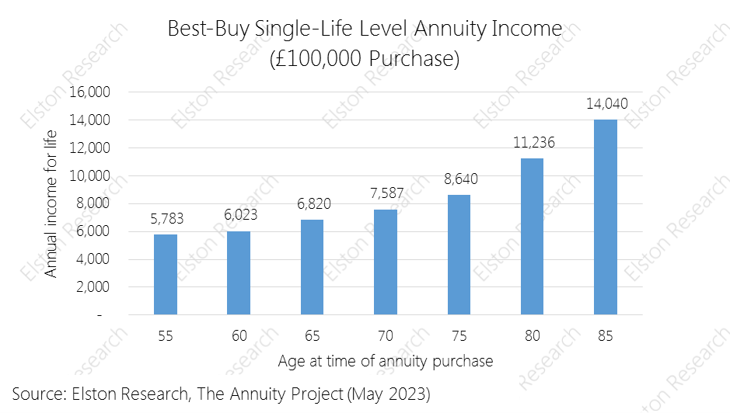

The Annuity Glidepath means offering both, but sequentially. This means retirement income comes from drawdown first, and then progressively from annuities from age 70-75 or so, depending on a client’s needs, withdrawal profile and capacity for loss. Furthermore, rather than considering a single annuity purchase, the Annuity Glidepath means offering a “ladder” of annuities purchased in stages as clients age. This approach means capturing better later-life annuity rates, as well as reducing the interest rate timing risk associated with a single annuity purchase.

The Annuity Glidepath framework can integrate with retirement portfolios on any platform, and gives advisers the flexibility to obtain quotes from any annuity provider, both on- and off-platform.

Elston Consulting’s Retirement Portfolios and Annuity Glidepath framework are available for licensing to DFMs and Financial Advisers.

Our Retirement Income Solution is designed to assist DFMs and financial advisers offer a comprehensive retirement income solution to their clients as part of their Centralised Retirement Proposition.

The Annuity Glidepath blends a purpose-built retirement portfolio in drawdown with a ladder of later-life annuities to create a blended retirement income solution for clients, as part of a Centralised Retirement Proposition.

When considering retirement income recommendations, advisers have been faced with considering recommending either drawdown or an annuity. Now it’s not an either/or decision.

The Annuity Glidepath means offering both, but sequentially. This means retirement income comes from drawdown first, and then progressively from annuities from age 70-75 or so, depending on a client’s needs, withdrawal profile and capacity for loss. Furthermore, rather than considering a single annuity purchase, the Annuity Glidepath means offering a “ladder” of annuities purchased in stages as clients age. This approach means capturing better later-life annuity rates, as well as reducing the interest rate timing risk associated with a single annuity purchase.

The Annuity Glidepath framework can integrate with retirement portfolios on any platform, and gives advisers the flexibility to obtain quotes from any annuity provider, both on- and off-platform.

Elston Consulting’s Retirement Portfolios and Annuity Glidepath framework are available for licensing to DFMs and Financial Advisers.