In this series of articles, I look at some of the key topics explored in my book “How to Invest With Exchange Traded Funds” that also underpin the portfolio design work Elston does for discretionary managers and financial advisers.

Aligning investment strategy with objectives Investing can be defined as putting capital at risk of gain or loss to earn a return in excess of what can be received from a risk-free asset such as cash or a government bond over the medium-to long-term. There can be any number of motives for investing: it could be to fund a future retirement via a SIPP, or to fund future university fees via a JISA. Online tools and calculators can help estimate how much is required to invest today to fund goals in the future. Investors can target a particular return, but learn to understand that the higher the required return, the higher the required level of portfolio risk. Risk and return are the “ying and yang” of investment. You can’t get one without the other. Total return can be broken down into income yield (dividends from equities and interest from bonds) and capital growth. In the UK, income and gains are taxed at different rates. If investing within a tax-efficient account, like a SIPP or an ISA, then income and gains are tax-free. If investing outside a tax-efficient account, investors must also then consider in their objectives how they want to receive total return – with a bias towards income or with a bias towards growth. Given the majority of DIY investors are able to make use of tax-efficient accounts, there is less need to consider income or growth, with many investors opting to focus on Total Returns and to use funds that offer “Accumulating” units that reinvest income, and reflect a fund’s total return. How then to build a portfolio to deliver an appropriate level of risk-return? What matters most when investing? For the purposes of these articles, I assume that readers need no reminder of the basic checklist of investing: to start early, to maximise allowances, keep topping up regularly, and to keep costs down. Then comes the key decision – what to invest in. The main driver of portfolio risk and return is not which stocks or equity funds are within a portfolio, but what the proportion is between higher risk-return assets such as equities, and lower risk-return assets such as shorter duration bonds. Put simply, whether to invest 20%, 60% or 100% of a portfolio in equities, will have a greater impact on overall portfolio returns, than the selection of shares or funds within that equity allocation. For example, when making spaghetti Bolognese, the ratio between spaghetti and Bolognese impacts the “outcome” of the overall meal, more than how finely chopped the onions are within the Bolognese recipe. While this may seem obvious, it gets lost in all the noise and news that focuses on hot stocks, star managers and performance rankings. For those that want to back up common sense with academic theory, the academic articles most referenced that explore this topic are Brinson Hood & Beebower (1986), Ibboton & Kaplan (2000), and Ibbotson, Xiong, Idzorek & Cheng (2010), all referenced and summarised in my book. Building a multi-asset portfolio to an optimised asset allocation to align to a particular risk-return objectives sounds like hard work and it is. That’s why multi-asset funds exist. The rise of multi-asset funds As investing becomes more accessible to more people, there is less interest in the detail of how investments work and more interest in portfolios that get people from A to B, for a given level of risk-return. After all, there are fewer people who are interested in the detail of how engines work than there are who are interested in how a car looks, how it drives and what they need it for. There is nothing new about multi-asset funds, indeed one could argue that the earliest investment trust Foreign & Colonial Investment Trust, founded in 1868, invested in both equities and bonds "to give the investor of moderate means the same advantages as the large capitalists in diminishing the risk by spreading the investment over a number of stocks”. In the unit trust world, managed balanced funds have been around for decades. I would define a multi-asset fund as a strategy that invests across a diversified range of asset classes to achieve a particular asset allocation and/or risk-return objective. They offer a ready-made “portfolio within a fund” thereby enabling a managed portfolio service for the investor from a minimum regular investment of £25 per month. . In this respect, multi-asset funds help democratise investing, and make the hardest part of the investor’s checklist – how to construct and manage a diversified portfolio. The different types of multi-asset fund available is a topic in itself. The ability for investors to select a multi-asset fund for a given level or risk-return characteristics for a given time frame is one of the most straightforward ways to implement a strategy once that has been aligned to a given set of objectives. Multi-Asset Fund or ETF Portfolio? The main advantage of a ready-made multi-asset fund is convenience. Asset allocation, and portfolio construction decisions are made by the fund provider. The main advantages of an ETF Portfolio are timeliness, cost and flexible. ETF Portfolios are timely. You can adjust positions the same day without 4-5 day dealing cycles associated with funds – an important feature in volatile times. ETF portfolios are good value. You can construct a multi-asset ETF portfolio for a lower cost than even the cheapest multi-asset fund. ETF Portfolio are flexible – you can tilt a core strategy to reflect your views on a particular region (e.g. US or Emerging Markets), sector (e.g. healthcare or technology), theme (e.g. sustainability or demographics), or factor (e.g. momentum or value), to reflect your views based on your research. Conclusion Setting the right objectives to meet a target financial outcome, such as funding future retirement, university fees, or creating a rainy day fund is the primary consideration when making an investment plan. Getting the asset allocation right – choosing a risk profile – in a way best suited to deliver that plan is the second most important decision. Finding a straight forward to deliver that risk-return profile, by building your own ETF portfolio or using a ready-made multi-asset index fund, is the final most important step. All the while, it makes sense to stick to the investing checklist: to start early, keep topping up, and keep costs down.  In this series of articles, we look at some of the key topics explored in my book “How to Invest With Exchange Traded Funds” that also underpin the portfolio design work we do for discretionary managers and financial advisers.

From space pens to pencils There’s a famous story, probably an urban myth, about NASA spending millions of dollars of research to develop a space pen whose ink could still flow in a zero gravity environment. When the Russians were asked whether they planned to respond to the challenge to enable their cosmonauts be able to write in space, they answered “We just use a pencil.” Sometimes sensible and straightforward answers to problems prove more durable than more elaborate and costly alternatives. The same could be said of investments. The quest for high-cost star-managers in the hope of alchemy, is under pressure from low-cost index funds that get the job done, by giving low cost, transparent, and liquid exposure to a particular asset class. How an active stock picker became a passive enthusiast I spent my early years in the City working for active managers. My job was to pick stocks based on proprietary models of those companies’ operating and financial models. I was fortunate enough to work in a very successful hedge fund, whose style was “true active”: it could be highly concentrated on high conviction stocks, it could be long or short a stock or a market, it could (but didn’t) use leverage. If you enjoy stockpicking, as I did, working for a relatively unconstrained mandate was at times highly rewarding, at times highly stressful and always interesting. Investors, typically large institutions, who wanted access to this strategy, had to have deep pockets to wear the very high minimum investment, and the fund was not always open for new investors. It certainly wasn’t available to the man on the street. Knowledge gap entrenches disadvantage When I started my own family and started investing a Child Trust Fund I became all too aware of the massive disconnect and difference between the investment opportunities open to hundreds of institutional investors and those available to millions of ordinary individual retail investors. I was staggered and rather depressed to see how few people in the UK harness the power of the markets to increase their long-term financial resilience. Of the 11m ISA accounts held by 30m working adult, only 2m are Stocks and Shares ISAs. The investing public is a narrow audience. The vast majority is put off from learning to or starting to invest by complexity, jargon and unfamiliarity. Casual conversations with people from all walks of life showed that whilst they may fall prey to some scheme that promised unrealistic returns, they were less inclined to put a “boring” checklist in place to contribute to their own ISA or Junior ISA, perhaps unaware that this could be done for less than the cost of a coffee habit at £25 per month. The lack of knowledge on investing was nothing to do with gender, age or education. It was almost universal. People either knew about investments or they didn’t. And that knowledge was usually hereditary. And it entrenches disadvantage. Retail investments need a shake up Looking at the retail fund industry, it was clear that there wasn’t much that was truly “active” about it. Most long-only retail managers hugged benchmarks for chunky fees that befitted their brand or status (now known as “closet indexing”). Until recently, the bulk of personal finance pages and investment journalism was more about a quest for a handful of “star managers”, in whatever asset class, who were ascribed the status of an alchemist, that investors would then herd towards. It seemed like the retail fund industry was focused on solving the wrong problem: on how to find the next star manager, rather than how to have a sensible, robust diversified portfolio. By contrast, in the US, there has always been a higher culture of equity investing (New York cabbies talk more about stocks than about sport, in my experience). So I was fascinated to read about the behavioural science that underpinned the roll out of automatic enrolment in the USA in 2005 where investors who were not engaged with their pensions plan were defaulted into a Target Date Fund – a multi-asset index fund whose mix of assets changes over time, according to their expected retirement date. I also read about the mushrooming of so-called “ETF Strategists”, investment research firms that put together ultra-low cost managed portfolios for US financial advisers built entirely with Exchange Traded Funds. Winds of change Conscious of these emerging trends, it seemed that mass market investing in the UK was about to enter a period of structural change: namely with the ban of fund commissions (Retail Distribution Review), and the launch of automatic enrolment, as well as other planned “behavioural finance” interventions to improve savings rates and financial capability. So in 2012, I set up my own research firm to see what, if any, of that experience in the US might apply in the UK. We work with asset managers to develop low-cost multi-asset investment strategies for the mass market, constructed with index-tracking funds and ETFs. It is bringing the rather dry science of institutional investing into the brand-rich and personality-heavy world of personal investing. Why index investing? I try and avoid the terms active and passive and will explain why. For most people, a multi-asset approach using index funds makes sense. This can be called “index investing”. Surprisingly, one of it’s biggest supporters is Warren Buffett. “Consistently buy a low cost…index fund. I think it’s the thing that makes the most sense practically all of the time…Keep buying through thick and thin, and especially through thin.” (Warren Buffet, Letter to shareholders, 2017) In this series of articles, I share some of the experience I have had in developing investment strategies and products for asset managers built with index funds and ETFs. I look at the concepts underpinning multi-asset investing, focus on the importance of getting the asset allocation right for a given objective, summarise my view on the active vs passive debate (and attempt to clarify some terms), as well as some practical tips on building and managing your own portfolio. Each of the articles can be explored more deeply in a book I wrote with my former colleague and co-author Shweta Agarwal on How to Invest with Exchange Traded Funds: a practical guide for the modern investor

Traditionally, UK pension fund managers and UK private client managers alike would have a bias towards home (i.e. UK) equities. Why is this, what does the research say and what does recent experience show? Understanding “home bias” First of all, what do we mean by home bias? We define home bias is allocating substantially more to the investor’s “home” market, relative to its capitalisation-based weight in a global equity index. Given the UK’s weight in global (developed markets + emerging markets) equity indices is now approximately 4% (it has been on a steady drift lower), any allocation above that level can be considered a home bias, from a UK investor’s perspective. Yet traditionally UK pension schemes and private client managers would split an equity allocation between broadly 50% UK and 50% international (ex-UK) equities. This represents a massive home equity bias, with a UK weight that is over 10x its market-cap based weight. Why does this home bias exist? The reasons given for such a massive home bias are typically the following:

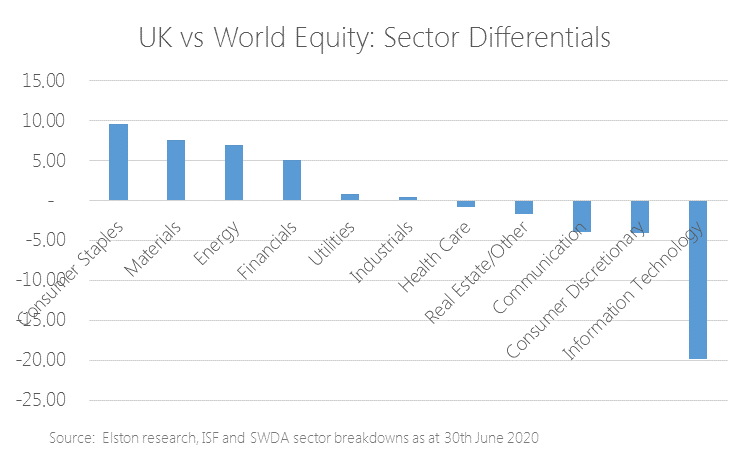

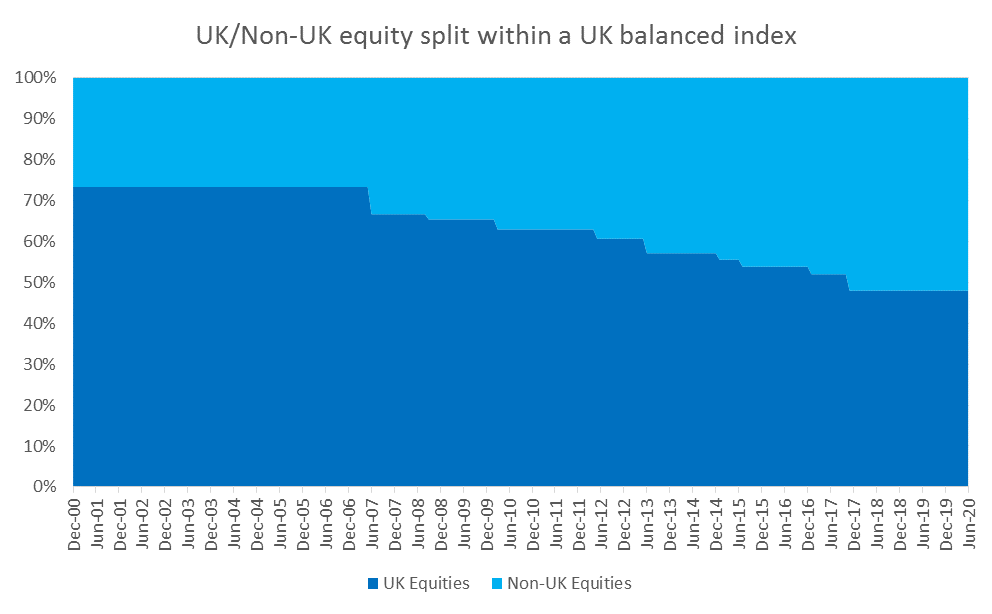

We can look at each of these in turn. Firstly, we would argue that investing in equities is not for currency/liability matching, but for return seeking and inflation beating: in which case, the broader the opportunity set, the greater the potential for returns. Put differently, a UK only investor is not only wilfully or accidentally ignoring 96% of the opportunities available in equities, by value, but would also thereby miss out almost entirely on the technology revolution led by US companies, for example, or the demographic revolutions of emerging markets. So whilst a home bias makes sense for a bond portfolio (matching changes in inflation and interest rates), a home bias for equities does not. Secondly, whilst the largest UK companies within the FTSE 100 are indeed “global” in nature, the broader, and more diversified (by sector and constituents), all share index is not. Furthermore the sector allocation of the UK market is skewed by domestic giants, can be out of step with the sector allocation for world equity markets. A UK equity bias is therefore a structural bias towards Consumer Staples, Materials and Energy, and a structural bias against Information Technology. Fig. 1. Sector Comparison UK Equities relative to World Equities  Thirdly, whilst it is indeed true that UK managers will be able to get more access and insight to UK companies than, say, an overseas-based manager, for portfolio managers who focus on asset allocation over security selection, this access to management is less relevant and less valuable. Whilst we can debate the detail of all three of these arguments, they are not individually or together enough to justify an allocation to UK equities that is over 10 times its market weight. This is not a question of a rational overweight, it’s simply an irrational bias. What does the research say? There has been extensive research into why individual investors and professional managers have a preference for creating an equity portfolio with a strong home bias[1]. French & Porterba (1991) observed the predominantly home equity bias of investors based on the domestic ownership shares (as at 1989) of the largest stock markets. In each case the high domestic ownership of each respective market implies a high home equity bias at that time: US (92.2%), Japan (95.7%), and the UK (92%), for example. In 1990 UK pension funds held 21% of their equity allocation in international equities from just 6% in 1979 (Howell & Cozzini 1990). Now the figure could be closer to 50%, or even higher. The shift away from home equity bias has been steady and pronounced in the UK institutional market, but is still ingrained. However, it’s worth noting that subsequent home bias research is written in the US. Given the US represents approximately 66% of the world equity market (a share that has been steadily increasing), the central tenet of that research is that home-biased US managers miss out on the diversification benefits and increased opportunity set available from investing in markets outside the US. Hence home-bias for a US manager creates a smaller “skew” vs Global Equities than it does for a UK manager. What is current practice? Whilst the institutional UK managers have been gradually reducing home bias within equity allocations, what about UK retail portfolio managers? We looked at the MSCI PIMFA Private Investor Indices[2] – and predecessor indices – to gain an insight as to what current asset allocation practice looks like for UK-based managers in the retail market. These weightings of these indices are “determined by the PIMFA Private Indices Committee, which is responsible for regularly surveying PIMFA members and reflecting in each index the industry’s collective view for each strategy objective”[3]. Based on the “Balanced” index (and predecessor indices[4]), within a typical balanced mandate, the allocation within the allocation equities have decreased from a 70/30 UK/international split in 2000, to a 48/52 split today (see Fig.2.). Whilst this reflects a reduction in the home equity bias, it is nonetheless a material bias towards UK equities by retail investment managers. Fig.2. UK/international equity split within an indicative UK retail balanced mandate  Source: Elston research, FTSE data, MSCI data In fairness, PIMFA has responded to this through the creation of a “Global Growth” index, which is 90% allocated to developed markets, and 10% allocated to emerging markets – so no UK home bias at all: but this is also a different risk profile to the Growth Index (100% equities, rather than 77.5% equities). Zimbabwean investors go global – UK investors should too We would make the case to advisers that if you were advising someone who lived in Zimbabwe, gut instinct would suggest that having the bulk of their equity allocation in Zimbabwean equities would feel like a poor and restrictive recommendation. After all, Zimbabwe makes up only a fraction of the global equity market. Without wanting to do UK plc down, the same gut instinct should apply to UK equities. If the UK is only 4% of global equities – why allocate much more than that? If you believe in equities for growth, it follows you believe in global equities to access that growth. Clients benefit from being shareholders in the changing mix of the world’s best and largest companies, not just the local champions. What does recent experience showing This debate was largely confined to theory given the relative stability of GBP to USD prior to Brexit. But given the dramatic currency weakness on the Brexit referendum, and the UK’s lack of exposure to the technology “winners” from the COVID-19 crisis, the disconnect between UK and Global Equity performance could not be more acute. Over the 5 years to 30th June, the FTSE All Share has delivered an annualised return of +2.87%p.a. in GBP terms, and MSCI World has delivered +7.53%p.a. in USD terms. That represents the difference in the performance of the underlying securities within those markets. Adjusting for currency effect too, and MSCI World has delivered +12.79%p.a. in GBP terms: an approximately 10ppt outperformance annually for 5 years. When expressed, in cumulative terms, the disconnect is more clear: over the 5 years to 30th June, the FTSE All Share has returned +15.22% in GBP terms, and MSCI World has delivered +43.80% in USD terms, and +82.66% in GBP terms: a 67.44% cumulative performance difference between those indexes, and the ETFs that track them. Fig.3. World vs UK Equity performance, 5Y to June 2020, GBP terms  Source: FTSE All Share, MSCI World, Bloomberg data Delivering good portfolio returns is less about picking individual winners within each stock market, but making sure you have access to the right asset classes for the right reasons. Index funds and ETFs are a low-cost, liquid and transparent way of accessing those asset classes. UK multi-asset perspective From a multi-asset perspective, the performance difference between MSCI PIMFA Global Growth (100% equity, no home bias), MSCI PIMFA Growth (77.5% equity, with home bias) and other risk profiles is presented in Fig.4. below. Fig.4. MSCI PIMFA Private Investor Index Performance, 5Y to June 2020, GBP terms  Source: MSCI PIMFA Private Investor Indices (formerly WMA), Bloomberg data The choice whether to embrace a UK home bias or avoid it has been critical and material and the main determinant of differences between multi-asset portfolio and multi-asset fund performance. The lack of UK home equity bias, is one of the key underpins of strong performance of the popular HSBC Global Strategy Portfolios and Vanguard LifeStrategy range, for example. A question of design Our preference for avoiding entirely any UK home bias for equities (but not for bonds) underpinned the construct of multi-asset funds and multi-asset portfolios that we have developed with and for asset managers. End investors in those products have benefitted from that key design parameter. Whilst we welcome managers launching global-bias multi-asset portfolios – it’s a bit late in the day as it won’t help their existing clients stuck in UK equities claw back the foregone performance of the last 5 years. The irony is that one of the reasons for the persistence of home equity bias is sustained by asset allocation providers used by wealth managers to construct multi-asset funds and portfolios. A closer interrogation of those research firms’ methodologies, parameters and constraints is required to think what makes best sense for end investors. Take action Looking to create your own investment strategy? Watch|Copy|Adapt our research portfolios Notes

[1] French, Kenneth; Poterba, James (1991). "Investor Diversification and International Equity Markets". American Economic Review. 81 (2): 222–226. JSTOR 2006858 [2] https://www.pimfa.co.uk/indices/ [3] https://www.pimfa.co.uk/about-us/pimfa-committees/private-investor-indices-committee/ [4] We define the predecessor indices to the MSCI PIMFA Private Investor Indices as: MSCI WMA Private Investor Indices, FTSE WMA Private Investor Indices, FTSE APCIMS Private Investor Indices Notices Image credit: Lunar Dragoon Commercial interest: Elston Consulting is a research and index provider promoting multi-asset research portfolios and indices. For more information see www.elstonetf.com

What actually delivers performance? A portfolio’s asset allocation is the key determinant of portfolio outcomes and the main driver of portfolio risk and return. Ensuring the asset allocation is aligned to an appropriate objective is therefore key. Getting and keeping the asset allocation on track for the given objectives and constraints is how portfolio managers can add most value for their clients. What differentiates portfolio managers? There are no “secrets” to asset allocation in portfolio management. It is perhaps one of the most well-studied and researched fields of finance. Perhaps unusually for a competitive service industry, core know-how is not a barrier to entry. Anyone completing their Chartered Financial Analyst exam will have a comprehensive grounding in the principles of portfolio management. There are, in my view, three differentiating factors for discretionary fund managers.

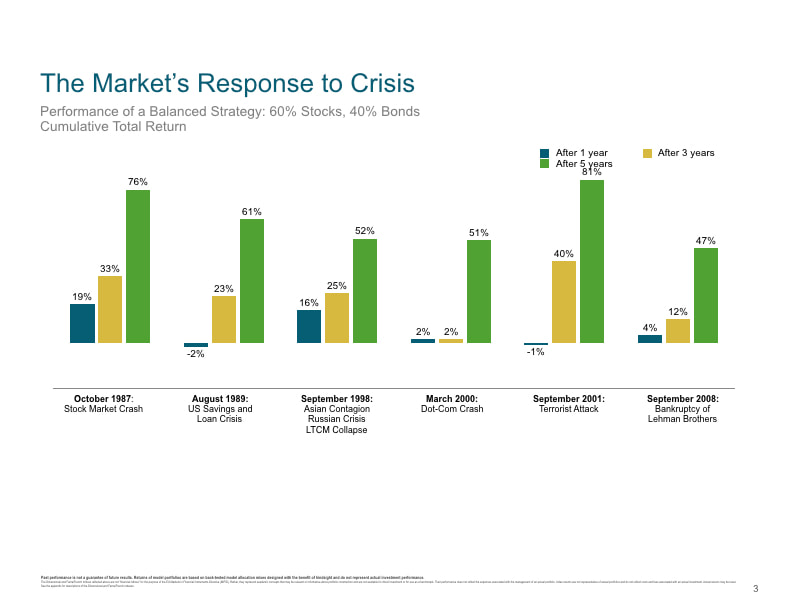

Quality of Process To create a quality investment process, managers need a robust set of capital market assumptions for each asset class and the relationship between asset classes. Ideally these should be term-dependent, to align to an appropriate term-dependent investment objective. To create an appropriate asset allocation, managers need to consider what their objective is: is it risk-adjusted returns in which an asset-optimised approach makes sense (the bulk of retail multi-asset strategies take this approach); is it to match future liabilities, in which case a liability-relative approach makes sense (more akin to how a defined benefit pension scheme is managed); is to target a volatility level or band; or is to target a level of income distribution. Managers also need to design a set of constraints – risk budget, fee budget, minimum and maximum position sizes, portfolio turnover constraints and counterparty considerations. Managers need to make implementation decisions as regards how they access particular asset classes or exposures – with direct securities, higher cost active/non-index funds, or lower cost passive/index funds and ETFs. Fund level due diligence as regards underlying holdings, concentrations, round-trip dealing costs and internal and external fund liquidity profiles are key in this respect. Quality of People Whilst we believe strongly in the deployment of technology to assist managers in designing, building and managing portfolios, that doesn’t mean that people aren’t core to a business. Investment managers must invest in their people to build on both quantitative skills that are necessary to finance as well as communication skills that are necessary to communicate with advisers and their clients. It’s people that make up a brand, and clients measure performance as much on client service as on returns. Quality of Proposition There are few firms, if any, that can build an end-to-end proposition entirely in-house. Part of a manager’s skillset is to understand where their expertise lies. We believe that there is little value in reinventing the various wheels of a proposition. But there is tremendous value in bringing together best in class components that create a proposition in a way that is robust, repeatable and proprietary. It’s the quality of choices around proposition that differentiate portfolio managers, and in this respect it is important to remain agile and adaptive, to a rapidly changing landscape in asset management and technology. Bringing it all together The objective for investment managers is no longer about “pushing” one product or another. It should be about providing solutions that help address a specific need. Managers should ask themselves: what problem is the investment strategy trying to solve for their client? How can they do that in a way that is robust, repeatable and evidence-based, so that everyone can sleep well at night? The secret is, there are no secrets. Good portfolio management is about focusing on what matters, using informed common sense.  Global stocks have been on something of a rollercoaster ride just lately, with markets trading at, or near, a two-year low. Doubtless many investors, especially those who are close to retirement, are feeling fearful. Fear is a hugely powerful emotion. It makes us do irrational things, and the sad fact is that, in the context of investing, there’s no shortage of people who want to take advantage. The Californian financial adviser and blogger Robert Seawright wrote an excellent article on this subject the other day. “When the markets are roiling,” he wrote, “fear is pitched all day, every day, and human nature buys it. And pays a premium. A very big premium.” “Fear makes money,” says Daniel Gardner in his book The Science of Fear. “The countless companies and consultants in the business of protecting the fearful from whatever they may fear know it only too well. The more fear, the better the sales.” So, what’s the answer, apart from steering well clear of salespeople? First things first: don’t feed the fear. When behavioural finance expert Greg Davies was invited on to Bloomberg to talk about the market rout in 2008, he was asked, live on air, what should investors if they’re really worried. “They should stop watching Bloomberg for a start,” he replied. Apparently, they tend not to invite him now. But, more importantly, investors who are anxious need to do some reading and arm themselves with an understanding of the bigger picture. To do it properly, it’s going to take you a little while. If you don’t have time, you could just watch a short video just released by Dimensional Fund Advisors, on how markets reward investors who stay disciplined at times such as these. The video is presented by DFA’s Vice-President and Head of Advisor Communication, Jake DeKinder. In the video, Jake says this: "Recent events have increased the feeling of uncertainty and may have led some to question whether to not to make changes to their investment approach. "It’s important to remember that while these events might seem frightening in the moment, they are not necessarily unique or unusual. “Throughout history capital markets have rewarded investors who are able to stay disciplined. After many major events, financial markets have recovered and delivered positive returns.” So what sort of events is Jake referring to? Well, here’s a series of graphs showing how a balanced portfolio comprising 60% equities and 40% bonds fared in the one, three and five years following the last six major market downturns:  What these graphs show very clearly is that those who stayed invested while so many others didn’t were amply rewarded on each occasion.

Here’s Jake DeKinder again: "Over the long term, investors who have been able to remain patient and tune out the short-term noise surrounding these events have been rewarded for doing so. “In the face of uncertainty, it’s important to remember this historical perspective, and focus on the things we can control, rather than the things we can’t.” If you’re in any doubt about what, if anything you should be doing, you should seek the help of a financial adviser. Otherwise, take Jake DeKinder’s advice: tune out the noise, think long term and disregard anything that’s out of your control. And most of all, fear not. Christmas is costly enough without baling out of the stock market. Here’s the Dimensional video: Dimensional Fund Advisors: Markets reward discipline  It’s almost that time of year when thoughts turn to resolutions for the 12 months ahead. Financial resolutions are always among the most common and, according to a poll by YouGov, the most popular resolutions in the UK this time last year included reading new books and learning a new skill.

For 2019, how about aiming to improve your knowledge of investing and personal finance through reading? No, we’re not talking about articles and blog posts, which only give you a tiny snapshot, but actual books which will leave you feeling that you’ve genuinely broadened your understanding. If that appeals, here are seven books we would recommend. THE BIGGER PICTURE The Geometry of Wealth: How to Shape a Life of Money and Meaning by Brian Portnoy Most people embark on an investment strategy without having a plan, and it’s not a good idea. True wealth, explains Brian Portnoy, is “funded contentment”. So, first of all, you need to work out what contentment looks like for you. What do you want from life? How much money do you need to enable you to lead that life? And when are you going to need it? Tackling these big questions and tending to everyday financial decisions, says Portnoy, are complementary, not separate, tasks. His book will help you to find the answers. The Financial Wellbeing Book by Chris Budd Personal wellbeing has almost become a new religion, but there are very few books that specifically tackle the financial aspect of it. In this book, former financial planner Chris Budd picks up on many of the issues discussed in The Geometry of Wealth. The starting point, he says is to “know thyself”. He then goes on to explain the secret to feeling in control of your finances, being able to cope with a financial shock and ensuring you always have options — and the peace of mind that goes with each of those. INVESTING The Little Book of Common Sense Investing by Jack Bogle Jack Bogle is the founder of Vanguard Asset Management, and the world’s most prominent advocate of low-cost index funds. This short, best-selling classic explains, in simple terms, how to guarantee your fair share of stock market returns by simply tracking global markets at minimal cost. The tenth anniversary edition has been updated and revised and is personally endorsed by none other than Warren Buffett. How to Invest with Exchange-Traded Funds (ETFs): A practical guide for the modern investor by Henry Cobbe & Shweta Agarwal OK, we’re not entirely impartial — Henry Cobbe is, of course, Elston Consulting’s Head of Research. But this book will particularly suit those who are looking to manage their own investments. It explains how to diversified and manage a low-cost, diversified and robust portfolio constructed entirely with ETFs. The Four Pillars of Investing by William Bernstein Learn about investing in just three books? Are we serious? Yes, we are. To quote William Bernstein in The Four Pillars of investing, “the body of knowledge that the individual investor, or even the professional, needs to master is pitifully small.” Bernstein’s book is a superbly written, down-to-earth and easy-to-read explanation of how to design an effective investment strategy and how to construct and manage an investment portfolio that reflects your personal capacity for risk. FINANCIAL HISTORY The Ascent of Money: A Financial History of the World by Niall Ferguson Uh? Why do you need to know about history to be financially savvy? Well, it’s true that history doesn’t repeat itself exactly, but having a very long-term perspective helps you to understand how financial markets work. “Sooner or later, says Niall Ferguson, “every bubble bursts (and) greed turns to fear.” But the good news is that capitalism has proved remarkably resilient over the centuries and, for patient investors, equities have delivered strong returns compared to cash and bonds. PSYCHOLOGY Thinking Fast and Slow by Daniel Kahneman What? How does a knowledge of psychology make you more financially literate? The answer is that, as the legendary investor Benjamin Graham once said, “the investor's chief problem – and even his worst enemy – is likely to be himself.” As Nobel laureate Daniel Kahneman explains, our minds are tripped up by error and prejudice, and investors are a classic example. His book includes a wealth of wisdom, as well as practical techniques for improving the decision-making process. Book lists are, of course, subjective. Books that we find helpful might not do the trick for you. Let us know how you get on with these, and if you have any suggestions for books we should add to future lists, we would love to hear from you.  All sorts of possible cures have been suggested for the ills of active fund management. Cutting fees is surely the most obvious solution if the industry wants to stem the flow of assets out of actively managed funds. Simply trading less frequently would probably make a difference too.

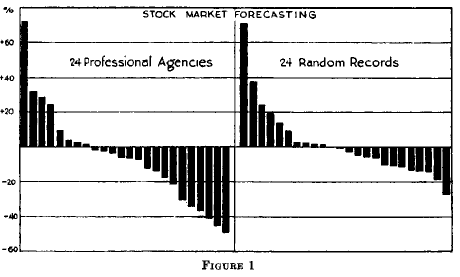

One of the arguments we frequently hear is that the answer lies in higher conviction, or “real” active management. It’s certainly true that the widespread practice of closet index tracking — charging active fees for effectively hugging the benchmark — is a big problem for the industry. As well as being fundamentally dishonest, it almost guarantees that, after costs, the investor will underperform a comparable index fund. “Real” active managers, on the other hand, genuinely try to beat the market by investing in a smaller number of stocks which they believe will outperform. Over the long term, only a tiny proportion of active managers outperform the market on a cost- and risk-adjusted basis — David Blake from Cass Business School puts the figure at around 1%. One thing those very few winners have in common, the evidence shows, is that they tend to be high-conviction managers with relatively concentrated portfolios. Understandably, then, the high-conviction approach is being heralded by some as the answer to the overwhelming failure of active managers to outperform. But is it? For a start, a manager can can have high conviction and yet be completely wrong. Deviating from the index doesn’t mean you’ll see better returns than the market; it means you can expect different returns, which could either be better or worse. New research by Tim Edwards and Craig Lazzara at S&P Dow Jones Indices suggests that far from solving active management’s problems, moving towards portfolios with fewer holdings may well exacerbate them. In a paper entitled Fooled by Conviction, Edwards and Lazzara suggest four likely consequences of active portfolios becoming substantially more concentrated, none of which makes comfortable reading for active investors. Likely Consequence No. 1: Volatility will probably increase Portfolios with a large number of holdings are less volatile than those with small number of holdings. So, for instance, if a manager reduces the number of stocks they hold from 100 to 20, the portfolio’s volatility will almost certainly increase. Likely Consequence No. 2: Manager skill will be harder to identify It’s already extremely hard to distinguish luck from skill in active management. Think of each stock pick as an opportunity for a manager to demonstrate their skill. The fewer stocks they pick, the bigger the impact that luck is likely to have on the outcome. Likely Consequence No. 3: Trading costs will rise There are two reasons, Edwards and Lazzara argue, why costs would probably rise with greater concentration. First, fund turnover would increase. Secondly, transaction costs per trade would also rise, because trading a higher percentage of the outstanding float in a security typically incurs a greater percentage cost. Likely Consequence No. 4: The probability of underperformance will increase Stock returns, in technical parlance, are naturally skewed to the right; in other words, the average stock tends to outperform the median. After all, a stock can only go down by 100%, but it can appreciate by more than that. Logically, then, portfolios containing fewer stocks will tend to underperform those with more stocks, because larger portfolios are more likely to include some of the relatively small number of stocks that elevate the average return. Conclusion So, what can we conclude from the Edwards and Lazzara paper? As the authors note, skilful managers sometimes underperform, and those who lack skill will sometimes outperform. “The challenge for an asset owner,” they conclude, “is to distinguish genuine skill from good luck. The challenge for a manager with genuine skill is to demonstrate that skill to his clients. The challenge for a manager without genuine skill is to obscure his inadequacy. Concentrated portfolios will make the first two tasks harder and the third easier.” Remember, S&P Dow Jones Indices is not a disinterested party in the debate about the rival merits of active and passive investing. It makes its money from licensing its indices for fund managers to use, and therefore has a vested interest in promoting passive strategies. That said, this latest paper is a valuable contribution to the discussion and one which gives advocates of higher concentration in particular plenty to think about.  What, one wonders, would Alfred Cowles III have made of the current “debate” about active and passive investing?

Cowles was born in 1891, the son of one of the founders of the Chicago Tribune. He became a successful businessman, but his true passions were economics and statistics. One question in particular exercised his mind — can the professionals predict the stock market? — and in 1927 he set out to find the answer. Over a period of four-and-a-half years, Cowles collected information on the equity investments made by the big financial institutions of the day as well as on the recommendations of market forecasters in the media. There were no index funds at the time, but he compared the performance of both the professionals and the forecasters with the returns delivered by the Dow Jones Industrial Average. His findings were published in 1933 in the journal Econometrica, in a paper entitled Can Stock Market Forecasters Forecast? The financial institutions, he found, produced returns that were 1.20% a year worse than the DJIA; the media forecasters trailed the index by a massive 4% a year. “A review of these tests,” he concluded, “indicates that the most successful records are little, if any, better than what might be expected to result from pure chance.” 11 years later, in 1944, Cowles published a larger study, based on nearly 7,000 market forecasts over a period of more than 15 years years. In it he concluded once again that there was no evidence to support the ability of professional forecasters to predict future market movements. What is so extraordinary about Alfred Cowles’ work, and the techniques he used, is how ahead of his time he was. Cowles was the first person to measure the performance of market forecasters empirically. Even among students of academic finance, the common perception is that it wasn’t until the mid-1970s that the value of active money management was seriously called into question, most famously by Paul Samuelson and Charles Ellis. In fact it was Cowles, more than 30 years previously, who first provided data to show that it was, to use Ellis’ phrase, a loser’s game. So why wasn’t Cowles’ research more widely known about? Why did it take until 1975 for the first retail index fund to be launched? And why is active management still the dominant mode of investing even now, in 2018? There are probably many reasons. The power of the industry lobby and the large advertising budgets at the disposal of the major fund houses have undoubtedly played a part, as has the growth of the financial media. But it was Alfred Cowles himself who put his finger on arguably the biggest factor behind the enduring appeal of active management. Late in life, Cowles was interviewed about his research into market forecasters. In Peter Bernstein’s 1992 book, Capital Ideas: The Improbable Origins of Wall Street, he is quoted as saying this: “Even if I did my negative surveys every five years, or others continued them when I’m gone, it wouldn’t matter. People are still going to subscribe to these services. They want to believe that somebody really knows. A world in which nobody really knows can be frightening.” Cowles’ prediction has proved to be spot on. Both active management and market forecasting are far bigger industries than they were when he died in 1984. Investors, it seems, still want to believe that the market can be beaten, despite all the evidence that no more fund managers succeed in doing it than is consistent with random chance.  Think of investing, and most people think of the financial market. They think of share prices going up and down, bull runs and bear markets, spectacular successes and the occasional market crash.

The media is partly responsible. Journalists are constantly looking for stories. They have a vested interest in making investing seem exciting. That’s why they love the drama of the stock market. Every day, newspapers publish the prices of hundreds of securities, and there are regular updates on radio and television on the latest news from the trading floor. The impression given is that investors need to keep up with the markets, and what the experts are saying about them, constantly. The truth, however, is rather more prosaic. Successful investing is essentially very dull. It’s about filtering out the noise and focusing on a few fundamentals — ensuring you’re taking an appropriate amount of risk, keeping your costs low and diversifying broadly. Apart from rebalancing your portfolio every year or so, there really isn’t anything else to do. In The Little Book of Common Sense Investing Jack Bogle wrote that “the stock market is a giant distraction from the business of investing”. In the long run, he explained, “investing is not about markets at all (but) about enjoying the returns earned by businesses.” This is an altogether better way to think about investing. At a basic level, it’s about sharing in the profits of capitalism. Companies distribute those profits in the form of dividends, generally paying higher dividends when they’re doing well, and lower dividends when they’re not. The price of shares in a particular firm tends to go up when the market expects its profits to rise, and down when profits are expected to fall. That’s why the stock market constantly fluctuates, and why, in the short term, it can be extremely volatile. Sensible investors, however, take a long-term view. No, they’re not blind to risks such as global warming, terrorism and the threat of nuclear war. But they believe that, in general, capitalism is a system that works and that fairly rewards those who invest in in. They believe in the resilience of human enterprise and that, whatever happens in the next 30, 40 or 50 years, there will still be a demand for goods and services, and that companies will continue to make profits. You should see investing, then, as claiming your rightful share to the proceeds of global capitalism. Remember, though, that there are all sorts of third parties — fund managers, brokers, investment platforms and so on — who would like to grab part of your share for themselves. Warren Buffett told a story in his 2006 letter to Berkshire Hathaway shareholders, which every investor should read. It concerns the Gotrocks family, which owns all of corporate America, and receives the full value of the profits earned by those companies. Then a group of people, which Buffett calls the Helpers, offer to assist some family members to outsmart the others, "for a fee, of course". So, while the total profit earned by the Gotrocks family doesn't change, they don't get it all, having to pay some to the Helpers. The profit of the companies owned by the Gotrocks family doesn't increase, but with more and more Helpers, charging more and more fees, the Gotrocks actually end up worse off. Buffett’s right. There are too many Helpers in the investing industry. By removing multiple layers of “help”, which you can do by simply using low-cost index funds, you’ll end up keeping a much larger share of your investment returns for yourself. So, go ahead. Claim your share of the proceeds of capitalism for yourself. It’s there for the taking — if only you can keep a long-term focus and resist the temptation to get caught up in all that market excitement.  One of the many reasons for indexing is that it eliminates, at a stroke, one of the biggest risks that active investors face, namely manager risk. We’ve explained many times how the odds of beating the market through active fund selection are heavily stacked against you. Speaking in the online documentary Investing: The Evidence, Dr David Blake from the Pensions Institute says this: “The evidence shows, both for the UK and the US, that around 1% (of funds) outperform in the long term on a risk- and cost-adjusted basis. 99% of fund managers deliver negative value-added once you take into account the fees that they charge.” All right, let’s say you’re feeling lucky, or else you don’t believe Dr Blake when he says that picking “star” managers ex ante is “impossible”. Let’s just imagine, for a moment, that you do possess a skill that has eluded every investor, professional or otherwise, to date — namely the ability to identify in advance, accurately and consistently, that tiny proportion of future outperformers. Even then you would still be relying on factors that are totally beyond your control. Let’s take, for example, the bond fund manager Ian Spreadbury, who has just announced his retirement after more than 40 years in the City of London. (Incidentally, the case for active management in fixed income is even flimsier than it is for equities. Because bond returns are generally modest, the costs involved in using an active manager almost always cancel out any outperformance they’re able to deliver. But we’ll leave that to one side.) The biggest problem active investors face is distinguishing luck from skill. In a paper released in 2002, the afore-mentioned David Blake and his colleague Allan Timmermann demonstrated that it takes 22 years of performance data for a test of a fund manager’s skill to have 90% power. Ian Spreadbury began his working life as an actuary. It wasn’t until 1985, nine years after graduating, that he moved into fund management with Legal and General. By Blake and Timmermann’s calculations, it wouldn’t have been until 2007 that you could say, with 90% confidence, that Spreadbury was genuinely skilled, as opposed to just plain lucky. By that time, Spreadbury had spent 12 years with his next employer, Fidelity. So, how has Spreadbury’s flagship Fidelity MoneyBuilder Income fund performed since 2007? Answer: it has consistently underperformed the benchmark index. In other words, you would have been better off investing in a low-cost passive fund instead. What’s interesting is that throughout that whole period, Fidelity MoneyBuilder Income has been highly rated by the ratings agencies. Brokers like Hargreaves Lansdown have also touted the fund in the media, predicting that Spreadbury would soon return to his winning ways. As things turned out, it didn’t happen — and nor will it happen now that Spreadbury has decided to call time on his career. We don’t mean to single out Spreadbury for criticism. He has, in fact, performed less badly, on average, since 2007, than his peers. But we do mean to call out those who advocate switching in and out of different active funds as a sensible investment strategy. Spreadbury is just another example of a fund manager who produced a few years of outperformance and earned considerable publicity for it and yet wasn’t able to sustain it. Once again, investors who poured into his fund on the back of all the fuss that was made have ended up disappointed. Manager risk is a very real risk. Even if a manager is skilled, and that’s a huge assumption to make, there are so many unknowns. Here are just a few of them: Will they be able to replicate their past success in the future? Will they struggle, as many do, as the size of the increases? Will they charge higher fees when they outperform? Will you have the discipline to stick by them during inevitable periods of prolonged underperformance? Will they move to a different fund? And in that case, should you follow them? Will they succumb to a serious illness or critical injury? Will they really want to carry on working into their 60s, by which time they’ll be financially very well off? As an active investor, you leave everything to chance, and to succeed at it, you need everything to go your way. As an indexer, you pay a tiny fraction of the cost and yet you’re guaranteed to receive, near enough, the full market return, for as long as you need to. Active management is a loser’s game, but one which the industry spends hundreds of millions of pounds every year persuading you to play. Don’t do it! It’s a game that only they can win.  Many of the decisions that investors typically make are way beyond their circle of competence. That’s the view of GREG DAVIES, Head of Behavioural Finance at Oxford Risk. In this interview, Gregg addresses two of the most prevalent behavioural biases investors are prone to — overoptimism and overconfidence — and argues that investors need to be much more realistic about which decisions they are sufficiently competent to make. Greg’s specialist expertise is in improving financial decisions through behavioural science. As well as holding a PhD in Behavioural Decision Theory from the University of Cambridge, he’s an Associate Fellow at Oxford’s Saïd Business School and a lecturer at Imperial College London. Greg Davies, in your view, how much of a problem do overoptimism and overconfidence pose to investors? A lot of investors could be characterised as passive-aggressive. They’re passive in the sense that they leave far too much of their wealth doing nothing for far too long, and with the wealth that they do put into the market, they are aggressively trying to do something to it at any given moment. When you’re trying to do something to your investments, then overconfidence and overoptimism becomes a problem. We all start to believe our own stories. For example, I read something in the newspaper, it resonates with me, I ascribe to it immediate and great confidence, and so I act on it. If we’re overconfident, we’re acting on stories that we shouldn’t be acting on, where we simply aren’t justified in having that level of confidence to do anything. You mentioned newspapers there. To what extent are these behaviours encouraged by what we read in the media? We ascribe information to things that we want to believe, so things that resonate with us we will start to believe more and more in. People will pick up and listen to all manner of things, including horoscopes at the extreme. No one ever acts, by the way, on numbers; no one buys return trade-offs. What we buy are stories, and stories come with a degree of comfort attached to them. If I have a story that is intelligible to me, if I understand it, if it just seems intuitively right, then it creeps past my guard, and the minute it is past my guard, it becomes something that I’m comfortable believing and something that I want to believe and so I become overconfident in it. How then should investors view fund or share tips or other recommendations they read about in the money pages or on the internet? If you were to look at all the possible decisions in front of you, some of them will be things where you genuinely have the knowledge to tell whether it’s a good or a bad decision. Warren Buffett talks about things being within your circle of competence. But some of the decisions in front of you will not fall in your circle of competence. They will be on the fringes of your competence. You might think you know something about them. The more decisions you make, the larger the proportion of decisions that aren’t going to be in your core sphere of competence. They’re basically decisions in which you’re just going to be rolling the dice. If we’re trying to make good decisions in investing, after fees and after all the noise in the markets, we shouldn’t be rolling the dice on marginal things. We should be acting only where we really have confidence and competence. A simple solution, surely, is for investors to make fewer decisions and just do less? Depending on who you talk to, people will have a different answer to the question, How much should you trade to do well in the markets? There are people at one end of the spectrum who will say their favourite holding period is for ever, and here are some people who think you have to trade a lot. Wherever you are on that spectrum the right answer is less than you think it is. However much you are inclined to do, a sensible investor always does less than that. The problem is though that it can be very tempting to try to time the market. It’s sometimes very hard to do nothing. When markets are going up and down, it normally feels uncomfortable for us to do nothing, not to react when it seems intuitively right to do so — for example, when the market is falling and you want to get out. It’s actually very difficult for us not to act on those sorts of things. The fact is though that this is the area where overconfidence manifests itself most extremely — our tendency to think we know where things are going next. In any short or medium time frame, the simple answer is that we do not know. The simple answer is, don’t do it. Focus on time in the market rather than timing the market. But it’s one of those things that’s simple but not easy. It’s simple to say it, but when it comes to that moment, it’s normally very emotionally uncomfortable for us not to act on what we feel to be strong information, so we jump in. There’s an example from animal behaviour, isn’t there, that you like to use to illustrate the value of staying in the market. Talk us through that. Yes, it’s from a study involving pigeons. You put the pigeons in a cage and they learn to peck a red light or a green light. When they peck the red light, it delivers food with a probability of 40%, and when they peck the green light, it delivers food with a probability of 60%. So these pigeons start to do things we see humans do. It's what’s called probability matching. They actually peck the green light more, because they get the food more frequently. They peck the green light 60% of the time and the red light 40% of the time. That seems all very smart and clever until you realise you that the optimal strategy is to peck the green light all of the time. Now, interestingly, that 60:40 gap is about the same as you would expect to see major equity indices posting on a monthly basis. About 60% of months the index goes up and about 40% of months it goes down. If we could predict which months it’s going to go up or down, it would be rational to switch between being in the market and out of the market. The fact that we can’t means that we should just keep pecking the green light, because that is the most rational thing to do, unless you have a crystal ball.  Vanguard Asset Management is one of the companies that’s helping to change the face of investing. Based in the US, it came to the UK in 2009, and last year it launched a direct-to-retail operation, allowing investors with as little as £100 to invest each month to access a range of low-cost funds. In this interview, Vanguard’s Head of UK Retail Sales NEIL COWELL explains why the company places so much emphasis on the importance of controlling costs, and discusses whether or not investors should use a financial adviser. Neil Cowell, as a company, Vanguard is always emphasising the importance of fees and charges. Why is controlling costs such a key component of successful investing? That’s right, we talk a lot about cost at Vanguard, and the importance of cost in investor returns. I think in the world of investing it can be said that you get what you don’t pay for. And costs do create an inevitable gap between market performance and investor return. The evidence is very clear when you look at the data. There’s data from Morningstar, for example, that clearly show that low-cost funds outperform their high-cost counterparts, and that alone gives a real indicator of why we attach such importance to it. In fact, Morningstar actually uses cost as a major predictor of a fund’s future performance, so every which way you look at it, costs are extremely important to investor outcome. It’s not an easy message to get across to investors though, is it? In almost every other area of our retail lives, the more you pay the more you get. That’s absolutely right. It’s counterintuitive. Clients definitely associate higher cost with higher quality and, as I said at the start, in the world of investing you get what you don’t pay for. When people see a fund priced at 1% per annum and another fund alongside it priced at 50 or 60 basis points, it doesn’t seem a lot in terms of a differential. But when that is actually compounded over time, it plays a terrific part in the overall return and takes quite a significant chunk from the final value. How important is it, would you say, for people to have a financial adviser? We’re very clear at Vanguard that clients are better served by working with an adviser. We spend a lot of time promoting the value of advice. We have a framework here that we call Adviser’s Alpha, which talks specifically around the value that an advised relationship will deliver over and above what a client left to their own devices may achieve. For a great investing outcome clients are well served by working with an adviser. We don’t say that clients who have the time, willingness and ability to self-serve can’t achieve a great outcome too, because that’s certainly possible. We just say it’s hard, and our message around the value of advice and what that adds is really very clear. From your point of view, then, what are the major ways in which a good adviser adds value? I think that there are two major parts. The first part is around the investment expertise itself, so the importance of getting the asset allocation right, the importance of rebalancing, the importance of ensuring that cost plays a part in portfolio construction. That does add value — there is no doubt about that. We rarely see portfolios that are constructed by clients themselves with a balance of equities and bonds, for example. They tend to resemble a collection of funds rather than a specific asset allocation. So there’s a real value add in the investment expertise element. But I think, going back to the Adviser’s Alpha framework, where an adviser can really add value is in their role as a behavioural coach or an emotional circuit breaker. We see time and time again that when clients are left to their own devices they can start to make some very costly mistakes. What are the most common mistakes you see people making when they try to manage on their own? We see for example investors typically chasing yesterday’s winners. They invest in what appear to be yesterday’s winning funds, expecting those funds to repeat the performance and to prevail for the next three, five, seven or nine years. There is a clear pattern. People also try to time markets, which is not an advisable thing to do. Typically we see investors get there too late, by which I mean there’s a big difference between the fund return and the actual return the investor experiences. So those are two examples, chasing yesterday’s winners and getting there too late, of behaviours that really do erode value. Another problem, of course, is that, in the words of your founder Jack Bogle, investors don’t “stay the course”. They bail out when markets tumble. And again, unadvised clients are more likely to capitulate. That’s right. At Vanguard we have what we call our investing principles. We believe that for a great investing outcome, investors should have a clear, articulated and definable goal. They need to understand why they’re investing in the first place. Alongside that we think it’s important to have an asset allocation that’s appropriate to their individual risk profile, and also to choose the component parts of that asset allocation at the lowest cost possible. But then comes the critical element. Having constructed the plan, having put the time and effort into getting that all right, you need to tune out the noise and keep your discipline. Markets will inevitably experience degrees of volatility. There is an inherent behavioural bias in all of us which is loss aversion, and it’s inevitable that clients will at least consider bailing out. That’s when the adviser really adds value. Jack Bogle also coined the phrase, “Don’t just do something, sit there”. In other words, expect the volatility, be confident in the plan, and ride it out, for great investing outcomes. What would you say to investors who think they can trust their ability to manage their own emotions and don’t need an adviser to do it for them? If that is the case, then maybe they are on of those investors who has the time, willingness and ability to self-serve. I think they’re rare, because most of us are subject to some of these behavioural biases. Carl Richards, who writes for the New York Times about behavioural biases, tells the story of when he was an adviser, the CEO of a Fortune 500 company came to him and asked him to run his personal affairs. He said to him, “Why are you asking me to do this? You know far more about investing than I do.” And the CEO said, “The reason I am asking you is because you’re not me.” It was the peace around that separation, that emotional circuit breaker, that he so valued. Where do you see the financial advice profession going in the future? I think at Vanguard we’re very clear that the need for advice is growing. We’ve seen data from the US and UK that shows the need is now greater than it’s ever been, and it's also very interesting that people are more prepared now than ever before, according to the data, to pay for advice. I suppose we shouldn’t be surprised about that given the dynamics. People are living longer, life is typically more complex, and people are now contemplating for the first time running their own retirement pots rather than being able to rely on an employment discretionary benefit scheme or final salary scheme. There are so many reasons why people see advice as more important now, and it’s encouraging to see that coming through in the data. Do you think some UK advice firms might feel a little threatened by Vanguard’s direct-to-retail offering? That’s a good question. I don’t think it was a particular secret that Vanguard would at some point introduce a direct offering. The reaction from our adviser community has been very positive. A lot of them are interested in the extent to which there may be access for advisers at some point. We’re nowhere near that, and it may never happen, but nonetheless the interest is there. So I don’t think there has been a bad reaction to it. I’ve been very encouraged over the last two or three years to see advice firms getting better and better at articulating their overall proposition. And I think that’s the key. Advisers these days are building more and more of their value proposition around their role as that financial coach, that behavioural coach, and no direct offering in the world can be a substitute for that.  A big problem for many investors is their overconfidence. They have unrealistic expectations about their own abilities at picking stocks and timing the market, and about the results they’re likely to achieve.

Bent Flyvbjerg is a professor at the Saïd Business School University of Oxford. An economic geographer, he’s an expert on behavioural economics and so-called optimism bias. His particular specialism is the planning fallacy — the tendency to underestimate the length of time and the expense involved in completing major tasks. But he also has a strong interest in how overconfidence impacts on investors. Although Professor Flyvbjerg admits to making small, and very occasional investments in individual stocks, he mainly uses index funds, and recommends that most investors do the same. He says it’s a lesson that he’s learned from being too optimistic about his own investments in the past. Thank you for your time, Professor Flybjerg. What exactly is optimism bias? Optimism bias is a propensity that humans have to look at the future through rose-tinted glasses, so to look at it in a more positive light than is actually warranted by what happens when the future gets here. That’s it in a nutshell. Why, then, are humans prone to optimism bias? There are a lot of theories about that, but the constant is that this is probably something evolutionary, that we need optimism to do what we do in life and to get up in the morning, to get married, to have children and go to work. This is something we assume that has been with humans for a very long time, that this is something we need to survive. It’s Darwinistic in that sense. It’s often very useful to be optimistic. You wouldn’t want a team of pessimists if you wanted to accomplish something. But optimism may also trip us up, so we might actually miscalculate risks regarding things that are very important. So you don’t want to get on a plane, for instance, when the pilot says he’s optimistic about the fuel situation. That’s not the kind of optimism that you want. But you do want to get on a plane where the flight attendant says that he’s going to give you a great trip, and they’re going to serve you great food and drinks and so on. How rife is optimism in the financial industry, in your view? It’s not just what I think. We know from solid research that it is very rife, it’s widespread, and it’s one of the things that you really need to guard yourself against as an investor — both your own optimism, and other people being optimistic with your money. That can lose you a lot of money. Give me a specific example, then, of how optimism bias can trip investors up, as you put it. Everybody hopes to have a windfall in the financial markets, and especially inexperienced beginners, who will think they’re going to be better than the average investor. People go into casinos and have this optimism where they’re going to beat the odds of the casino. The hardest thing to learn is not to be too optimistic. It’s really difficult. It takes a lot of time, and a lot of experience, and there are very few investors out there who have this cool realism that will make you successful as an investor. But it’s very tempting, isn’t it, not to act when we keep hearing in the media plausible arguments for buying this or that? Yes, it’s difficult not to get caught up in that, but it’s well documented that you shouldn’t listen to that kind of stuff. Day-to-day news on financial affairs is mostly noise. You need to look at much longer trends to get anything like useful information. You can always build a story around some random variation that sounds meaningful, and then you act on the basis of that and find that it’s not meaningful at all. It’s sometimes assumed that financial professionals are above these sorts of biases. What do you say to that? It’s not true. With professionals, there’s actually an additional bias — in addition to optimism bias — because they have a deliberate interest in making people believe they can do better. It’s what we call a strategic bias. Professional investment managers will try to make their clients believe that they’re better than the markets, and again it’s been shown that on average you’re better off without a professional investor than with one. You said it’s very difficult to combat optimism bias. But how can you make a start? The first thing to do is to realise that you have optimism bias. And of course, if you’re biased, you need to be de-biased. Experiments have been made on people who make decisions about things. One group is not told what the usual outcomes are, and the other group is told. So the second group will get a realistic image. They will think about that when they make their decision and will not be as biased as the first group. So just telling people what the empirical data are will make them less biased. But the real secret to getting bias out is not to make subjective decisions. You basically want to make decisions that are more or less automatic. So instead of trying to time the market you would say like, if you are investing, that I’m going to invest every three months on a specific date; I’m going to invest whatever I have at that moment. You’ll do better than if you try to save up your funds and figure out where the market is going and try to time the market. Optimism bias has to have an opportunity to kick in, right, and it’s only when we make subjective decisions that it kicks in. So the more you can eliminate those and go on autopilot, so to speak, the better off you will be in making investment decisions. But again, its hard to temper your optimism when you read about professional investors who’ve made successful call, isn’t it? There are so many things happening in the financial markets that there will always be stories like that, and that’s exactly what you have to disregard. Only if you see something that you really believe in and you were dead certain that it’s going to outperform the market would you be justified in doing something apart from just investing in something like the S&P 500. How has your research impacted on your own investment decisions? I actually try to use these ideas about optimism bias in my own investments. So I’m very conservative in that sense. (If you’re going to speculate) you should only put a little money on it — very small investments on things that have an enormous upside. By making a small investment you create a small downside. So you play on the large upside with a small downside, and the rest of your investments you just keep in the index. You invest in index funds yourself. Why did you decide to go down that route? Like many investors, I took a lot of time to learn this, and it cost me a lot of money. I did it because I saw that it was bulls**t (to suggest) that professional investment managers are performing better than the index. At the same time as I was developing my own experience as an investor this type of research became very well known in the early 2000s. Daniel Kahneman won the Nobel Prize in Economics for his research on optimism bias and the planning fallacy. That just showed me that you’re just giving money to other people instead of actually investing it and making money for yourself.  It’s no secret that active fund managers are losing business to index funds, but they aren’t going down with a fight.

The big fund houses have always had large marketing budgets, and they’re drawing especially heavily on them now. As the US blogger Dan Solin wrote recently, the rational choice for investors is simply to “buy a globally diversified portfolio of low management fee index funds”. The problem is, “there’s a huge industry spending hundreds of millions of dollars annually to persuade you not to. They’ll say almost anything to persuade you to hand over your hard-earned money to them.” But are the marketers getting desperate? Are they trying too hard to stem the flow of money out of active funds and into passive ones? There are signs that they might be. A good example is a new campaign by Allianz Global Investors, the asset management branch of the German insurance company Allianz SE. Alliance GI executives have been touring the company’s 14 offices around the world, handing out brand new pairs of training shoes to its staff. It might sound like a joke but it isn’t. Apparently it's designed to emphasise AGI’s belief in active fund management. Bloomberg quotes Andreas Utermann, AGI’s chief executive officer, as saying: “Sneakers are just part of this brand relaunch. It’s not just the investment process that’s active, it’s the whole ethos of the firm and the way that we give advice.” It is, of course, a huge gimmick. It plays on the conjunction fallacy — the common assumption that doing something is better than doing nothing, and that hard work and effort inevitably lead to better outcomes. In fact, it’s the activity that’s the problem. As the former fund house executive Lord Myners recently admitted, most funds perform better when the managers aren’t working at all (i.e. when they’re on holiday). Why? Because of the constant buying and selling that active managers feel they have be doing to justify their fees and bonuses and to keep their jobs. Every trade they make adds to the cost of using them, and as studies have repeatedly shown, cost is the single most effective predictor of future fund performance. As well as redoubling its marketing efforts, Allianz GI is also revisiting its fee structures in an attempt to woo new customers. It recently cut the management fee on some of its funds in return for a performance fee it only charges if the fund beats its benchmark. “You only pay if we perform,” says Utermann. “Why wouldn’t that be a good deal?” Unfortunately, though, funds with performance fees are not the no-brainer the fund industry likes you to think they are. OK, you don’t get charged if the fund trails the index, but nor do you get reimbursed the money that you would have made if you’d invested in a low-cost index fund. After costs, active funds underperform the index most years, often by large margins, and the performance of AGI funds over the years has been little or no better than those of its peers. Over time, the cumulative effect of that underperformance will leave a big hole in your returns. Add to that the compounded management fee (even if it is reduced), and having to pay additional performance fees when the fund does beat the market, and it all makes a for a very bad deal for consumers. Like the training-shoe stunt, performance fees are just a gimmick. Compared to the US, the indexing revolution in the UK is only just beginning, and we can expect to see active managers become increasingly desperate to cling on to their market share. However tempting their offerings sound, you’re almost certainly better off steering clear.  An Englishman’s home is his castle, the saying goes. But in truth, the Scots, Welsh and Irish are just as keen on owning their own home. And for many Brits, one home is not enough; the level of buy-to-let and second home ownership is higher in the UK than almost anywhere else in the world.